Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Yes, yes, everyone’s very excited about gold:

Sequential record highs for so-called analogue bitcoin have understandably been attracting a lot of attention, given normally what’s good for gold…

…is generally seen as bad for the world.

Over on Unhedged, our esteemed and dapper colleague Rob Armstrong has been writing about the rally for a while, and took a look at the metal’s mysterious new marginal buyers in today’s newsletter. He looked at several potential culprits:

— Jewellery demand

— Geopolitics

— Investors seeking cash alternatives

— Fiscal profligacy

Also gazing at the gold stuff is Bank of America, which in a note today posed the question “Is gold a safer investment than Treasuries?”.

Their most immediately relevant finding is that — after a long period of gains driven by Chinese demand — this is now a Western-led rally:

Flows have changed markedly in recent months. Indeed, China’s non-monetary gold imports fell from an all-time high in 1Q24 to multi-year lows over the summer, as the government signalled another round of monetary and fiscal stimulus, boosting equity markets. At the same time, Western investors stepped in, after holding back for a while as they waited for the Fed to kick-start the monetary easing cycle.

Notably, non-monetary market participants have increased their exposure on both the physical and paper markets, and our contrarian analysis suggests the latter is not overbought. Still, markets are also now factoring in a no-landing scenario for the US and a slower pace of rate cuts. This may curtail the potential upside near-term. There is also a risk that gold may give back some of the recent gains, although we ultimately see prices supported at $2,000/oz.

In terms of motives, BofA is firmly Team Fiscal Profligacy:

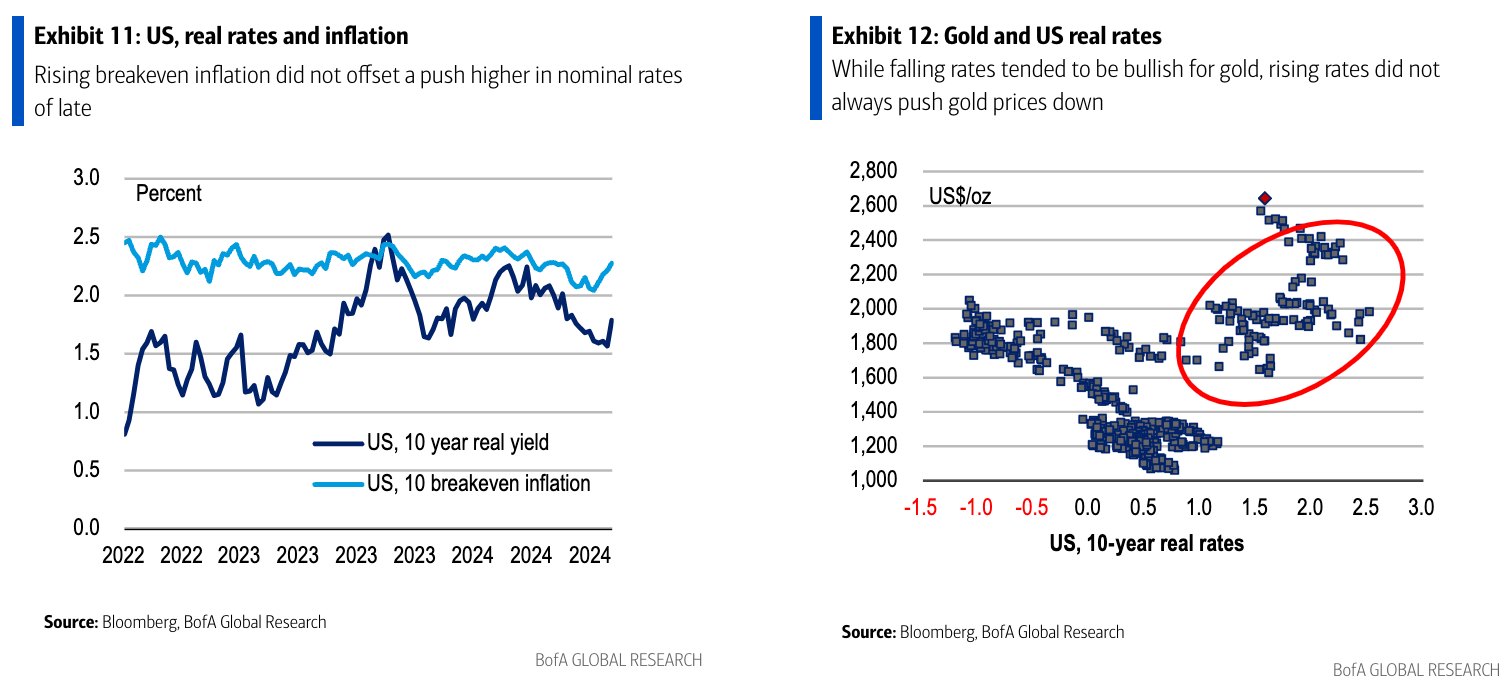

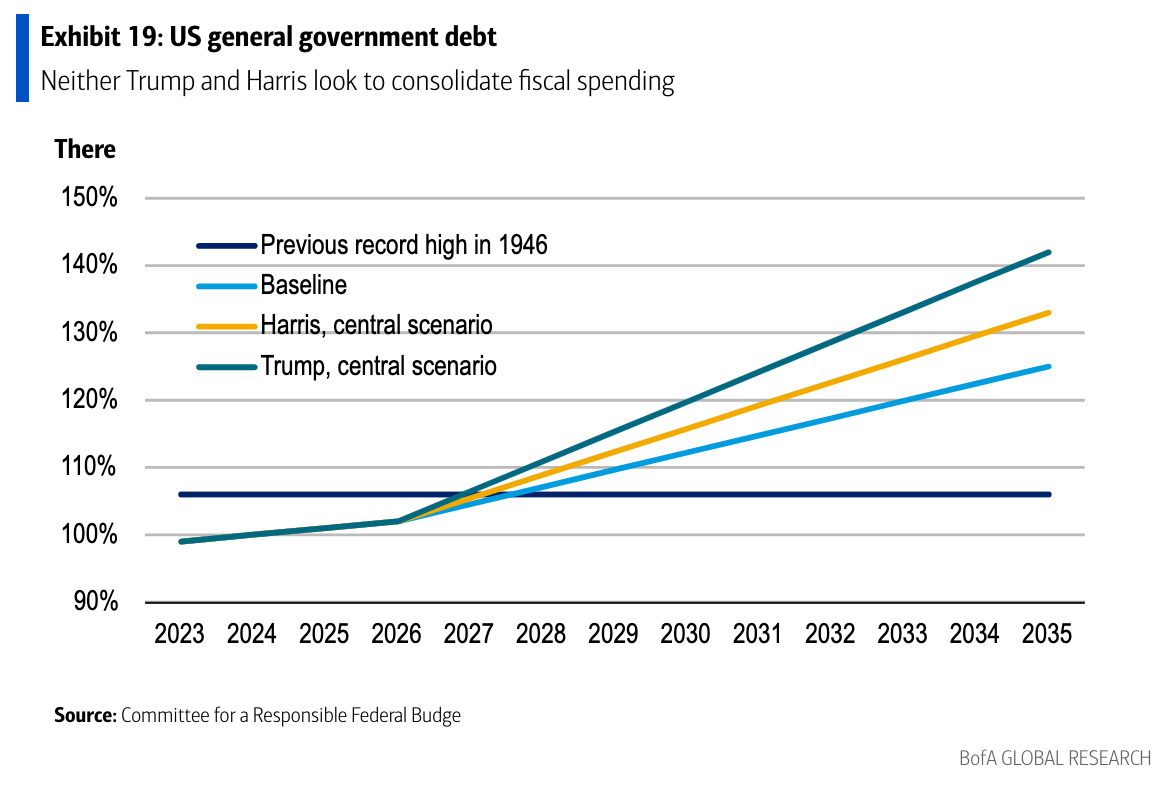

10-year real rates have historically been a critical gold price driver. Yet the correlation between the two assets has weakened: a decline in rates is still bullish, but higher rates do not necessarily put pressure on gold. This reflects a number of factors, not least concerns that fiscal policy in both the US and elsewhere may not be sustainable. Indeed, the Committee for a Responsible Federal Budget notes that the national debt is projected to reach a new record high as a share of the economy only three years from now, well within the next presidential term, pushing up interest rate payments as a share of GDP. In turn, this makes gold an attractive asset, so we reaffirm our $3,000/oz target. Indeed, with lingering concerns over US funding needs and their impact on the US Treasury market, the yellow metal may become the ultimate perceived safe haven asset.

(High-res)

{kind=link}

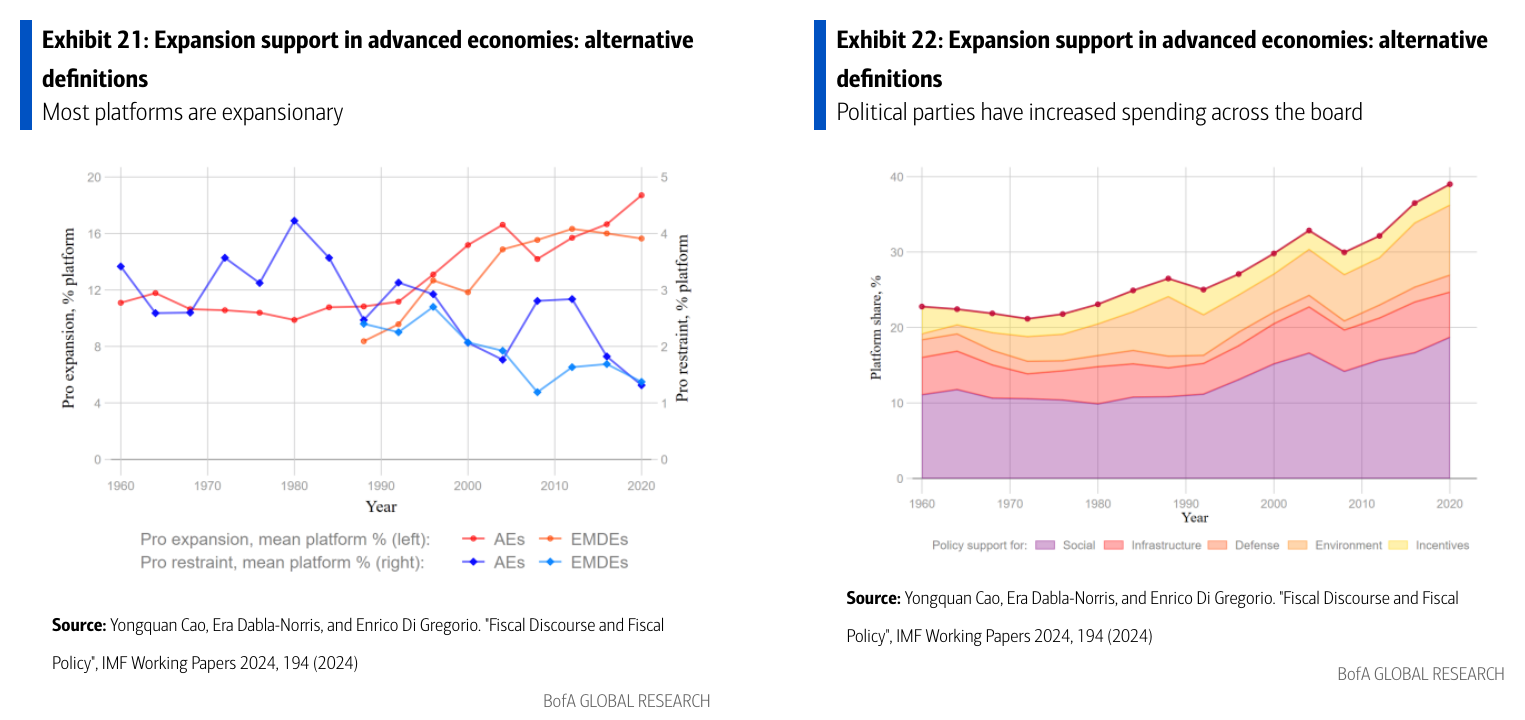

As spending and debt climb globally, this dynamic will only increase, BofA’ analysts reckon:

Neither Kamala Harris nor Donald Trump seem to prioritise fiscal consolidation, but the US is not alone. An analysis of policy platforms in advanced economies suggests policymakers strongly favour fiscal expansion… Central banks in particular could further diversify their currency reserves: the share of gold holdings is now at 10%, up from 3% a decade ago.

They add (our emphasis):

Spending commitments will in all likelihood increase, as countries adapt to and tackle climate change, demographics become more challenging and defence spending likely goes up. The IMF estimates that this new spending could amount to 7-8% of GDP annually on average for the global economy by 2030. Ultimately, something has to give: if markets become reluctant to absorb all the debt and volatility increases, gold may be the last perceived safe haven asset standing.

(High-res)

{kind=link}

(High-res)

{kind=link}

It’s an interesting possibility, and fits with the conventional goldbug argument: global debt is surging (hello, $100tn), and the gold long thesis follows that eventually this debt will have to be monetised, which will cause inflation, and gold will keep its value etc etc. If that argument appeals, more power to you: go buy some gold and just hope everybody keeps their nerve.

Does that make gold the ultimate safe haven investment? Well, no — that’s probably still a war rig, or a lot of tinned beans.

Further reading:

— Explaining the commodity warehouse trade with scripture (FTAV archives)