Oil prices dropped over 5 per cent yesterday after Iran’s Ayatollah Ali Khamenei over the weekend seemed to play down the prospect of re-re-re-re-re-re-re-retaliatory strikes against Israel:

With the risk of a full-blown war between the two states having abated for at least a few more minutes, attention among oil investors “is once again shifting back to market fundamentals,” JPMorgan analysts write.

There’s just one problem: OPEC’s relative opacity and China’s use of underground storage facilities mean few analysts, including those at America’s biggest bank, seem to know with much confidence what those “fundamentals” are.

“Forecasting future supply and demand in the current environment is a waste of time because we cannot even measure what’s happening in the present,” says Ilia Bouchouev, the former president of Koch Global Partners and an authority on all things oily. JPM commodities strategists Natasha Kaneva, Prateek Kedia and Cole Wolf admitted to their own confusion in a note on Monday. (“This makes me happy to hear,” Bouchouev winks.)

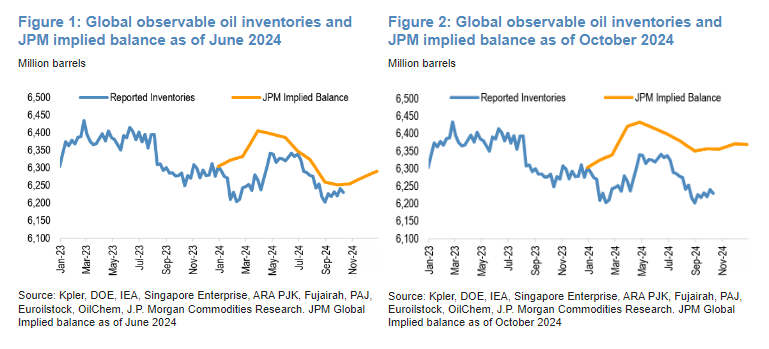

Back in June, the JPM trio said they expected global demand for oil liquids to exceed supply by about 1 million barrels per day, “with a sizable 1.9mbd deficit in August followed by a 0.3mbd deficit in September”. These forecasts were eventually “validated,” the analysts said — observable inventories fell by 117mn barrels globally during the summer months, and particularly quickly in August.

But it turns out the market may be far, far looser than JPM had initially thought. “With the incorporation of new data,” the analysts now think the third-quarter deficit was around 0.5mbd (rather than 1mbd), 0.9mbd in August (rather than 1.9mbd) and that the market turned to a 0.3mbd surplus in September (rather than a 0.3mbd deficit as previously forecast). That means there were roughly 45mn extra barrels around between June and September.

[High-res]

{kind=link}

What gives? From JPM’s note:

This contradiction might be explained by assuming that our projected supply is too high or that demand is too low. Alternatively, it could suggest that global observable inventories are being underreported.

The idea that their supply forecasts may have been too high seems unlikely, the strategists explain, particularly for non-Opec sources including the US, Brazil, Guyana, Canada, Argentina, Norway and Columbia. These countries account for three-quarters of non-Opec+ production, and all of them provide “reliable” monthly production figures, JPM says.

“Conversely, we might be overestimating OPEC supply, though this seems unlikely,” the bank adds.

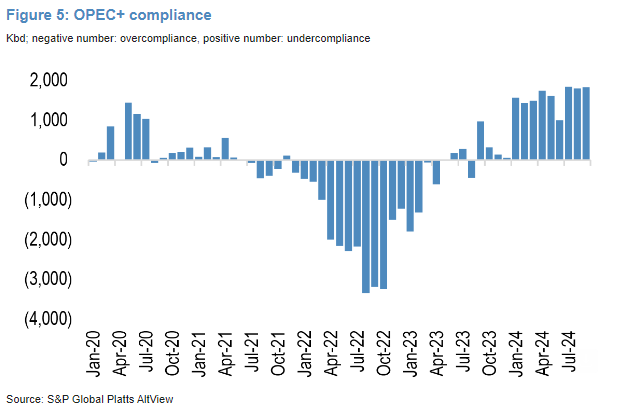

For our OPEC supply numbers, we rely on data from S&P Global Platt’s AltView. This approach uses supply-to-market data by combining crude/condensate export figures with internal refinery runs and crude burn estimates. It then subtracts any crude/condensate imports and/or blended diluent/fuel oil/NGLs from the exports.

For countries with more opaque reporting, data are further cross-checked with JODI, primary submissions to OPEC and other tanker tracking and proprietary sources. Notably, there has been significant undercompliance in 2024, with OPEC+ overproduction exceeding 1.8 mbd each month of 3Q2024, led by the UAE, Iraq, Kazakhstan and Russia, highlighting ongoing compliance challenges.

[High-res]

{kind=link}

Maybe JPM’s demand estimates were too low, then? “It’s possible,” they acknowledge.

Weaker-than-expected Chinese demand in the second and third quarters was effectively cancelled out by stronger-than-expected demand in the Middle East, where soaring temperatures meant more power was required to keep everyone cool.

Perhaps, though, Chinese demand (which may have already peaked, in historical terms, as the population begins to decline) isn’t as weak as analysts had assumed. When it comes to modelling total demand, you see, JPM and others look at three main measures: refinery output, net imports and stock changes for refined products . . .

— After “adjusting Chinese refinery runs and crude imports to account for Iranian and Venezuelan crude feedstocks entering China as fuel oil and blended bitumen,” JPM reckons that year-to-date, China’s processing rates averaged 15.3mbd. That’s 0.3mbd less than in 2023.

— China’s crude imports fell to 11.4mbd during the first nine months of this year. That’s 0.3mbd less than in 2023.

— However! Domestic production is up this year to 4.2mbd, from 4.1mbd in 2023.

— Combining domestic output with imports means China had a total of 15.6mbd available to process, “leaving a surplus of about 0.3mbd compared to the 15.3mbd available for processing”.

All of which, according to JPM, flies in the face of figures from data and analytics company Kpler that suggest Chinese crude stocks, including barrels in transit, have declined by 37mn barrels, or 0.14mbd, so far this year.

The discrepancy implies three things, JPM concludes:

-

It appears China is aiming to build a cushion of inventories, possibly as a precaution against potential disruption in crude shipments due to escalating tension in the Middle East or potential restrictions from a US administration

-

These crude stocks seem to be stored in underground storage facilities, invisible to Kpler’s satellites that track only above-ground storage.

-

China’s demand for crude could be underestimated by about 300 kbd given our belief that, when it comes to commodity inventories, what enters China, stays in China.

Bouchouev basically concurs. When it comes to estimating oil inventories, he says investors are groping in the dark:

Neither demand nor inventories are observable with any degree of accuracy that could impact prices, so if you are missing two out of the three components (i.e., Change in Inventories = Supply – Demand) then you cannot solve the problem and draw any meaningful conclusions. There are just too many different usages of petroleum products spread out across a zillion global locations, and way too many storage facilities where owners have no interest in disclosing the truth and more often even have incentives to mislead the observers.

Yes, China is the primary example and I don’t disagree with JPM’s three conclusions, which basically says that nobody knows.

Fortunately, prices today . . . are much more driven by flows and not by barrel-counters trying to reconcile their numbers, which I safely put into the noise bucket.

So that’s all cleared up then.

Further reading:

— Who and what is driving oil price volatility (FTAV)

— BP reports lowest quarterly profit since pandemic on weak oil prices (FT)