EUR/USD News and Analysis

Recommended by Richard Snow

How to Trade EUR/USD

ECB Officials Eye June Meeting for First Rate Cut, SNB Delivers a Surprise Cut

In spite of the glaring differences between EU and US growth prospects, ECB officials maintain a cautions approach to the inevitable rate cutting cycle – eying up June as the all important meeting. Wage growth has been a major focus from governing council members in 2024 but it looks like the ECB is running out of reasons to push back on interest rate cuts.

Earlier today, the Swiss National Bank delivered a surprise 25 bps cut in an attempt to normalize monetary policy. The was deemed necessary in light of a challenging external environment, real appreciation in the Swiss Franc and sub-two percent inflation which is likely to continue next year and in 2026.

Dollar Drop Appears Short-Lived as EUR/USD Heeds Resistance

Yesterday’s dovish Fed announcement allowed for markets to price out expectations of the Fed removing a full 25 basis point (bps) hike from its yearly outlook – sending the dollar lower.

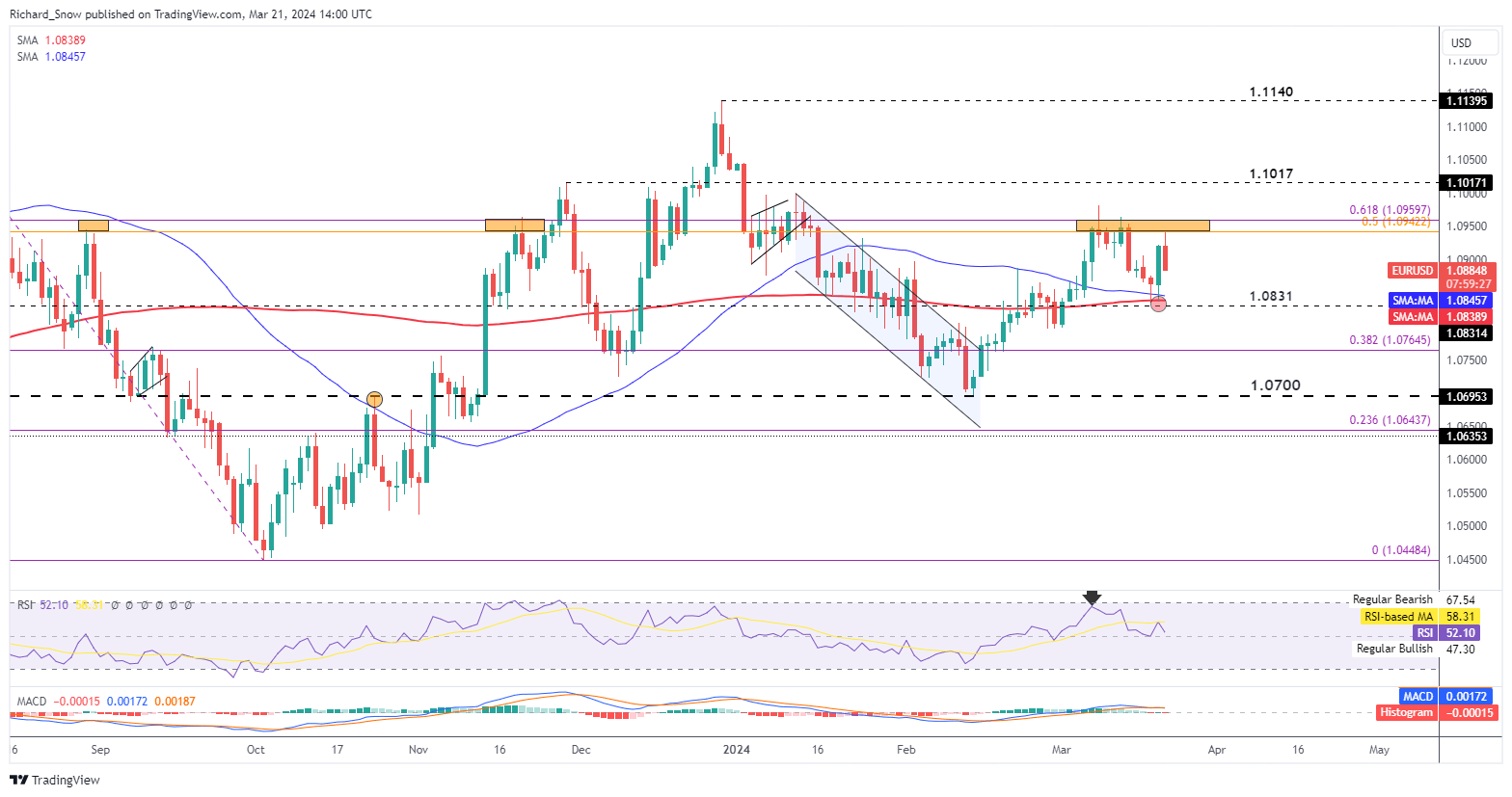

EUR/USD naturally benefitted from the momentary dollar depreciation and earlier today, tested the confluence zone of resistance around 1.0942 and 1.0960. The two levels correspond to the respective Fibonacci retracements involving the 2020-2022 major decline and the 2023 descent. Piece action highlights the 50 and 200-day simple moving averages (SMAs) and the 1.0830 marker as support.

EUR/USD Daily Chart

Source: TradingView, prepared by Richard Snow

| Change in | Longs | Shorts | OI |

| Daily | 11% | -18% | -2% |

| Weekly | 6% | -25% | -8% |

With a superior interest rate differential and a resilient economy, the US dollar is likely to remain supported – especially if incoming inflation prints continue to surprise to the upside as they have in some form or another since December last year. Another development in the summary of economic projections (SEP) was the consistent uprating of the Fed funds rate throughout the forecast horizon, including the rise from 2.5% to 2.6% for long-run estimates. This suggests a higher ‘neutral rate’ for the Fed in the face of resilient growth and a robust labour market.

Additionally, the European economy remains stagnant and in much need for accommodation, increasing the likelihood of a cut from the ECB – particularly if inflation continues to head towards the 2% target.

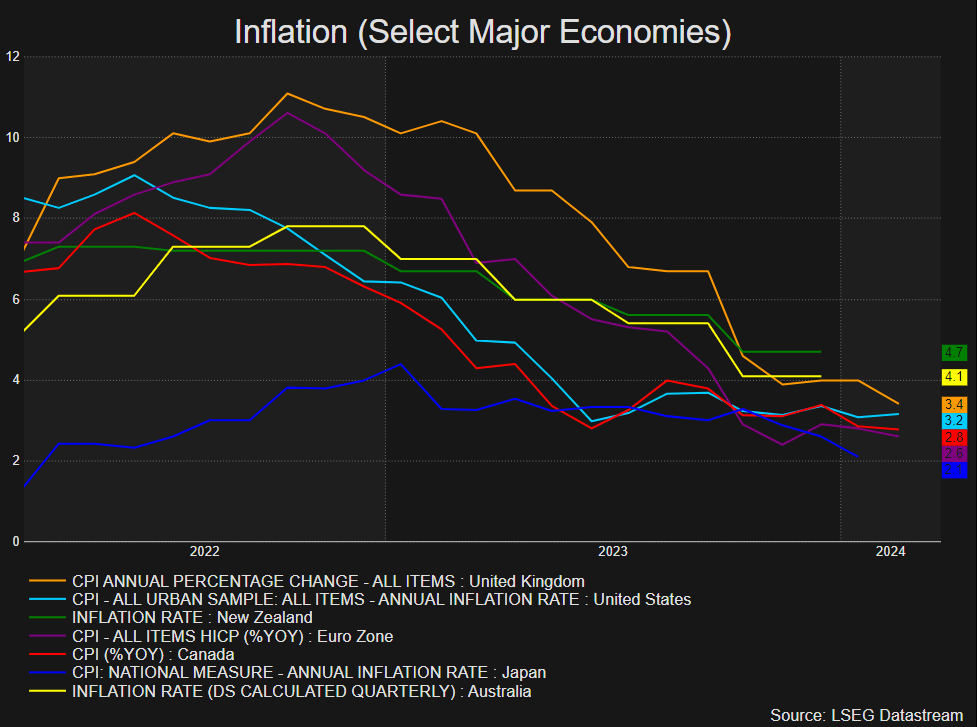

The chart below contrasts the path of inflation for major economies, highlighting the progress seen in the EU (purple). The figure used if the HICP but the CPI reading on 2.8% also suggests improvement in the rate of price increases year-on-year.

Source: Refinitiv Workspace, prepared by Richard Snow

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX